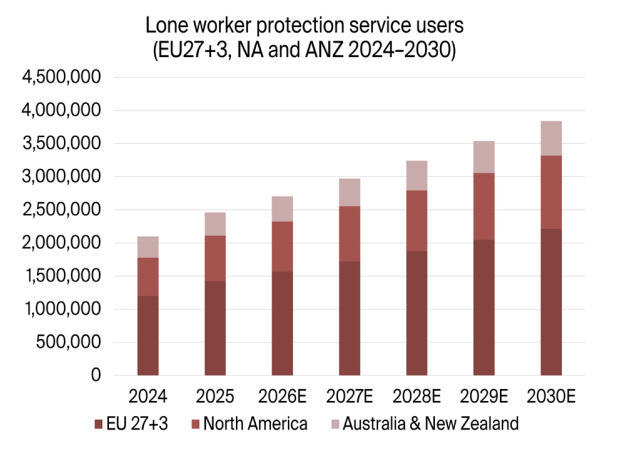

Berg Insight estimates 2.5 million people across Europe, North America and Australia & New Zealand were using connected lone worker safety solutions by the end of 2025, with steady growth projected through 2030. The data points to a market where apps are rising, but dedicated devices still matter for higher-risk deployments.

Lone worker safety has quietly become one of the most operationally consequential “people-centric” IoT segments: it sits at the intersection of compliance, real-time connectivity, and emergency response. The challenge is not simply adding a panic button to a phone. It is proving that alerts are raised reliably, located accurately, and handled by a workflow that an employer can defend after an incident.

New figures from analyst firm Berg Insight put some scale behind that reality. The firm estimates that the user base of connected lone worker safety solutions in Europe, North America and Australia & New Zealand reached 2.5 million at the end of 2025. In parallel, Berg Insight values the 2025 market for connected lone worker safety solutions and services at € 171 million in Europe, € 95 million in North America and 42 million in Australia & New Zealand.

Looking ahead, Berg Insight expects Europe to grow from 1.4 million users at the end of 2025 to over 2.2 million by the end of 2030, a 9.2 percent CAGR. North America is forecast to rise from 685,000 users to about 1.1 million over the same period, a 10.0 percent CAGR. Australia & New Zealand is projected to grow from 350,000 users to 520,000 users by 2030. Market value is also expected to expand: Europe is anticipated to reach € 251 million by 2030 and North America € 146 million; Australia & New Zealand is forecast to reach 59 million.

Apps are advancing, but the device debate is not over

One of the more telling takeaways is that the industry’s transition to app-based solutions is continuing, but not at the pace many platform vendors once assumed. Berg Insight notes that the shift has “slowed down slightly in recent years as employers in high-risk industries continue to prefer dedicated lone worker devices.”

This matters for IoT professionals because it frames a practical deployment trade-off: smartphone-based safety can reduce hardware overhead and speed rollouts, but it also inherits the variability of consumer devices, user behavior, and operating-system constraints. Dedicated devices—typically chosen when risk tolerance is low—signal that reliability, battery autonomy, ruggedness, and predictable alert behavior remain central purchasing criteria, even when an app-based alternative exists.

A fragmented vendor landscape, with a few scale players

Berg Insight describes a market served by a mix of hardware device suppliers, software providers, and alarm monitoring and response services, with only a few companies delivering complete end-to-end offerings. That structure is a key differentiator versus many other IoT application areas: value is not only in connectivity and device management, but also in what happens after an alarm is generated—triage, escalation, and response processes that often require 24/7 operational capability.

Geographically, the report highlights that many of the largest vendors originate from the UK, Canada and Australia—also identified as the three largest markets. In Europe, Berg Insight says UK-based Peoplesafe leads with around 375,000 subscribers. In Australia, Duress is described as the clear market leader with hundreds of thousands of subscribers. In Canada, the leading companies cited are Aware360, Blackline Safety and Tsunami Solutions, while AlertMedia and Becklar are named as major players in the US. Berg Insight also lists a long tail of notable vendors across the UK, Europe, and Australia & New Zealand, underlining how local regulation, service models, and buyer preferences continue to sustain regional ecosystems.

Why growth is holding—and where differentiation is emerging

According to Berg Insight analyst Melvin Sorum, demand is being driven by a familiar but potent mix: new lone worker safety regulations, the costs associated with employee injury and absence, increased awareness of lone worker risks, and efficiency benefits tied to protection services.

At the same time, Berg Insight points to intense competition, with commoditisation and price pressure shaping the market. The notable angle here is where differentiation is now expected to come from: the firm flags data analytics services built on lone worker device data and AI-driven preventive safety features as promising developments. In other words, vendors are being pushed to compete on outcomes—risk reduction, earlier intervention, and operational insight—rather than on the basic mechanics of sending an alert.

For OEMs and module suppliers, the persistence of dedicated devices keeps demand alive for purpose-built hardware designs rather than an all-app future. For connectivity providers and platform operators, the opportunity is less about raw SIM volumes and more about service assurance: coverage intelligence, roaming behavior, and the operational tooling to support devices and smartphones at scale. And for system integrators and enterprises, Berg Insight’s numbers reinforce a procurement reality: the “solution” is increasingly a blend of device/app choice, monitoring workflows, and analytics—making integration and operational readiness as decisive as the endpoint itself.

The post Connected Lone Worker Safety Users Reach 2.5M Across Europe, North America and ANZ in 2025 appeared first on IoT Business News.