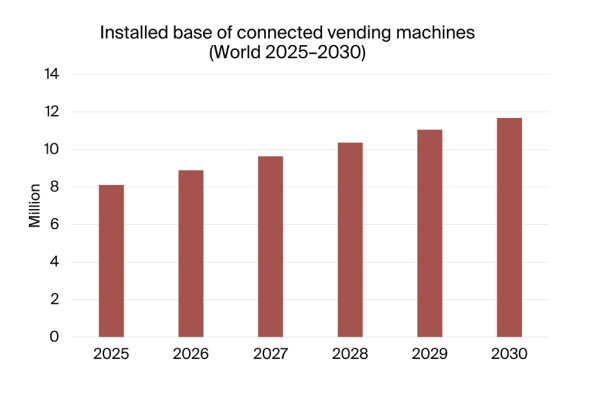

Berg Insight estimates 8.1 million connected vending machines were in operation globally in 2025 and projects the installed base to reach nearly 11.7 million by 2030, with cashless payment and newer “grab-and-go” formats reshaping what “vending” means.

Vending may look like a mature business, but its technology stack is being quietly rebuilt around connectivity. What started as basic telemetry—knowing whether a machine is stocked, powered, and functioning—has become tightly coupled to cashless acceptance, remote operations, and increasingly, on-screen merchandising. In that context, a new snapshot from IoT analyst firm Berg Insight puts some scale behind the shift: the global installed base of connected vending machines reached an estimated 8.1 million units in 2025.

The regional split is notable because it underlines where momentum is building. Berg Insight says “Rest of the World” represents the largest share, at around 3.3 million connected machines, driven primarily by rising volumes in China and Japan. North America follows with an estimated 2.6 million, while Europe stands at around 2.2 million.

Looking ahead, Berg Insight forecasts that the installed base will grow at a 7.6% CAGR to reach nearly 11.7 million connected vending machines by 2030. If that trajectory holds, connectivity will no longer be an add-on: global penetration is expected to reach 77.5% at the end of the forecast period.

Why this market is different from typical “connected device” growth stories

Unlike many IoT segments where connectivity is justified by operational efficiency alone, vending connectivity is increasingly pulled by a consumer-facing requirement: payment choice. Berg Insight calls out cashless payments as the main driver for adding connectivity, and notes that contactless payments—especially smartphone-based—have become ubiquitous at vending machines in many regions. That matters because the payment edge becomes the connectivity edge: once cashless acceptance is deployed, telemetry and remote management tend to follow as part of the same upgrade cycle.

Another differentiator is that the “device” being connected is not just a sensor endpoint. Berg Insight points to modern vending equipment such as payment devices and touchscreens that typically come pre-equipped with connectivity and telemetry functionality. This shifts the integration burden away from retrofitting entire machines and toward selecting and operating an ecosystem of peripherals and service platforms. A practical implication follows: solution selection is less about a single hardware SKU and more about lifecycle management across payments, connectivity, telemetry, and the operator’s back office.

A crowded vendor landscape, but with clear regional gravity

Berg Insight describes a market served by specialised technology companies providing connected vending telemetry and cashless payment solutions, alongside vending machine manufacturers and some large operators with in-house capabilities.

In terms of installed base, the report identifies US-based Cantaloupe and Israel-based Nayax as the largest providers, each with estimated installed bases in the range of 900,000 connected vending machines. Their footprints are structurally different: Cantaloupe is concentrated in North America, while Nayax is spread across North America, Europe, and Rest of the World markets—an important distinction for OEMs and integrators building multi-region rollouts.

Beyond the top two, Berg Insight lists Televend (INTIS), Ingenico, Vendon, Coges (Azkoyen Group), MatiPay, and InHand Networks as other major suppliers. Televend is described as the clear leader in Europe and is expanding in North America, suggesting that competitive dynamics may increasingly hinge on cross-Atlantic expansion as operators seek consistent tooling and reporting across regions.

On the manufacturing side, Berg Insight notes that Crane Payment Innovations (CPI) holds one of the leading positions globally, while LE Vending and TCN Group are important players in China. Among operators, Berg Insight highlights that most work with third-party providers, though some run in-house solutions—citing Chinese UBOX and Italy’s IVS Group through its subsidiary N-and Group as examples.

Touchscreens, digital signage, and the rise of “grab-and-go”

The most consequential takeaway may be that connectivity is enabling new vending formats, not just modernising old ones. Berg Insight points to touchscreens being used as digital signage to display nutritional information, advertisements, and targeted promotions—features that turn the machine into a managed media endpoint as well as a retail endpoint.

Meanwhile, micro markets and grab-and-go machines are reshaping the landscape. Berg Insight expects grab-and-go machines—such as smart coolers—to have a significant impact, noting that adoption has been particularly evident in China where they account for a large share of new installations, and that the concept is now gaining traction in Europe and North America.

One operational insight embedded in these trends: as the installed base approaches the penetration levels Berg Insight forecasts, the market’s growth will depend less on “connecting legacy machines” and more on what replaces them. Berg Insight explicitly frames grab-and-go as having the potential to replace a significant portion of traditional vending fleets in Europe and North America, which would shift procurement priorities toward platforms that can support new interaction models and product identification workflows rather than simple stock monitoring.

For OEMs, connectivity providers, and system integrators, the message is straightforward: connected vending is moving into a more platform-centric phase. Winning solutions will need to bridge payments, device management, and new retail formats—at global scale, but with clear regional differences in competitive positioning and deployment patterns.

The post Connected vending machines pass 8 million units as cashless payments accelerate adoption appeared first on IoT Business News.